When you’re trying to manage your money, some of the words used around borrowing can feel like another language.

APR? Interest? Credit commitments?

It’s no wonder people feel confused, and sometimes tricked, by credit agreements.

At IE Hub, we believe understanding your money shouldn’t feel intimidating. This blog breaks down the key terms around credit in a simple, easy-to-understand way, so you can make clearer choices and feel more confident.

What is credit?

Credit means borrowing money that you agree to pay back later, often with extra charges added.

Types of credit include:

-

Credit cards

-

Buy Now, Pay Later schemes

- Loans

-

Overdrafts

-

Catalogue accounts

-

Car finance

Each of these comes with a credit commitment, a responsibility to repay the amount borrowed.

What are credit commitments?

Your credit commitments are any repayments you’re expected to make regularly.

This could include:

-

Minimum monthly payments on a credit card

-

Weekly store credit instalments

-

Monthly car finance payments

-

Loan repayments

When budgeting, these go in the “should-pay” category, not quite as urgent as rent or food, but still very important. Missing payments can lead to extra charges, damage to your credit score, or even enforcement.

What is interest?

When you borrow money, you usually pay back more than you borrowed. That extra amount is called interest.

Think of it as the cost of borrowing. It’s how lenders make money.

For example:

If you borrow £100 and your interest rate is 10%, you’ll owe £110.

The higher the interest rate, the more you’ll repay overall, even if the loan or credit card looked like a “deal” at first.

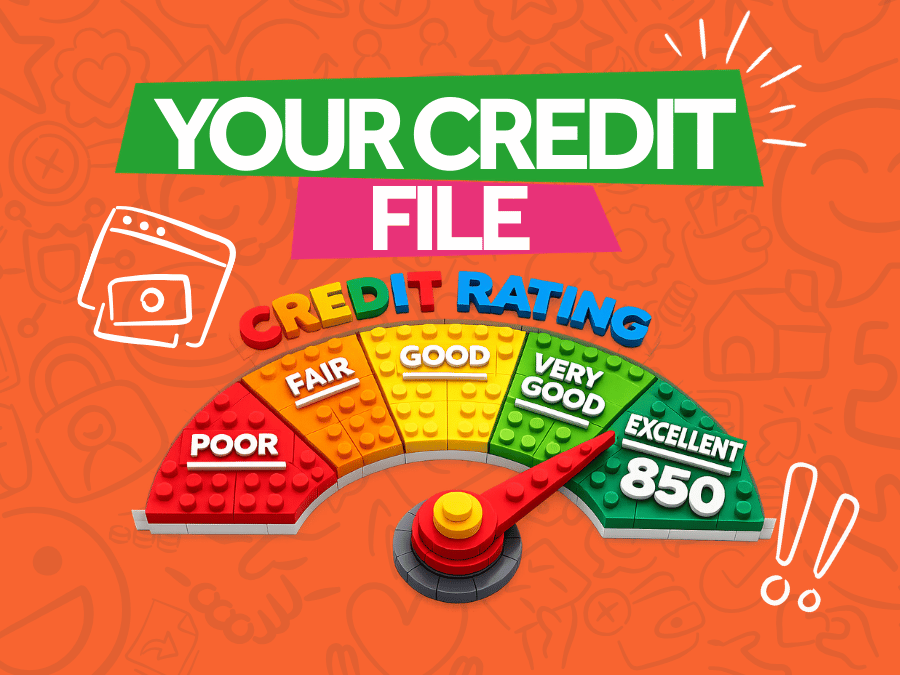

What is APR?

APR stands for Annual Percentage Rate.

It’s the total cost of borrowing money over one year, including:

-

Interest

-

Fees

-

Any extra charges

APR helps you compare different credit offers, even if they have different interest rates or payment structures.

The lower the APR, the cheaper the credit overall.

Be careful with “representative APRs.” This is just an example, not always what you’ll get. Your personal rate could be higher depending on your credit history.

Why this matters

Some credit deals are advertised as “affordable”, but when interest and fees are added, the total cost can be much higher than you expect.

This is how many people end up with long-term debt from short-term borrowing.

Understanding the real cost of credit means you can:

-

Avoid taking on more than you can manage

-

Spot when a deal isn’t as good as it seems

-

Choose credit that fits your budget

How IE Hub can help

When you use IE Hub to build your budget, you can include your credit commitments and get a clearer picture of your finances.

We help you:

-

List all your credit payments in one place

-

See what support you might be entitled to

-

Share your situation with companies safely and securely, without phone calls

- No judgement. Just clarity and support.

Useful support links

Final thought

Credit can be helpful when used carefully, but only when you understand what you’re agreeing to.

Knowing what interest and APR really mean puts you back in control. And if you’ve already taken on more than you meant to, there’s no shame, just support and next steps.

At IE Hub, we’re here to help you face it all, one clear step at a time.