Debt - a word that can stir up anxiety and confusion for many. Yet, it’s a fundamental part of personal finance that affects nearly everyone at some point in their lives.

Let’s break down what debt really means, why it matters, and how to manage it wisely, especially if financial terms like APR, Credit Score, Priority vs Unpriority and Credit Scores feel overwhelming.

Hear from an expert on how he perceives debt differently to us!

What is Debt?

At its core, debt is simply money borrowed with a promise to repay it later, usually with interest.

It comes in various forms, like credit cards, loans for cars or homes, or even student loans.

These are tools that help us afford big purchases or handle unexpected expenses when cash isn’t readily available.

Different Opinions and Perceptions

The way people perceive debt versus credit applies to the likes of credit cards, mortgages, retail finance, car loans, and other forms of borrowing.

Some people categorise any outstanding balance on these loans as debt, regardless of how well they manage their payments. They view it as a financial obligation that needs careful management to avoid potential risks.

In contrast, others see these financial tools as manageable credits, especially when payments are made consistently and on time. They may use mortgages to afford homes, retail finance for purchases, or car loans for vehicles, viewing them as necessary tools for achieving financial goals rather than problem debts.

This distinction reflects individual attitudes towards borrowing and financial responsibility across various aspects of personal finance.

Credit vs. Debt: Understanding the Difference

Credit

Imagine credit as a financial tool—a way to buy things now and pay for them later.

It’s like borrowing money from a friend and agreeing to pay them back after a while.

Debt

Debt, on the other hand, happens when we don’t manage credit responsibly.

Missing payments or borrowing more than we can repay can turn manageable credit into problem debt.

Problem Debt: When Does it Become an Issue?

People can fall into problem debt when they struggle to meet the financial agreements provided by their lenders. The main sign of this can be difficulties in managing repayments on loans or credit agreements.

Being in arrears means falling behind on payments, typically after missing one or more scheduled payments. This can trigger consequences such as late fees, and penalties, and negatively impact credit scores.

If left unresolved, accounts may move into default, where the lender takes further action to recover the debt. This could involve issuing formal notices, engaging debt collection agencies, or even legal proceedings.

Problem debt can happen from a combination of factors, including unexpected expenses, changes in income, or overspending beyond means.

Recognising early signs of financial strain and seeking assistance, such as through debt advice services or negotiating repayment plans with creditors, can help people regain control and prevent further escalation of debt issues.

Why Debt Management Matters

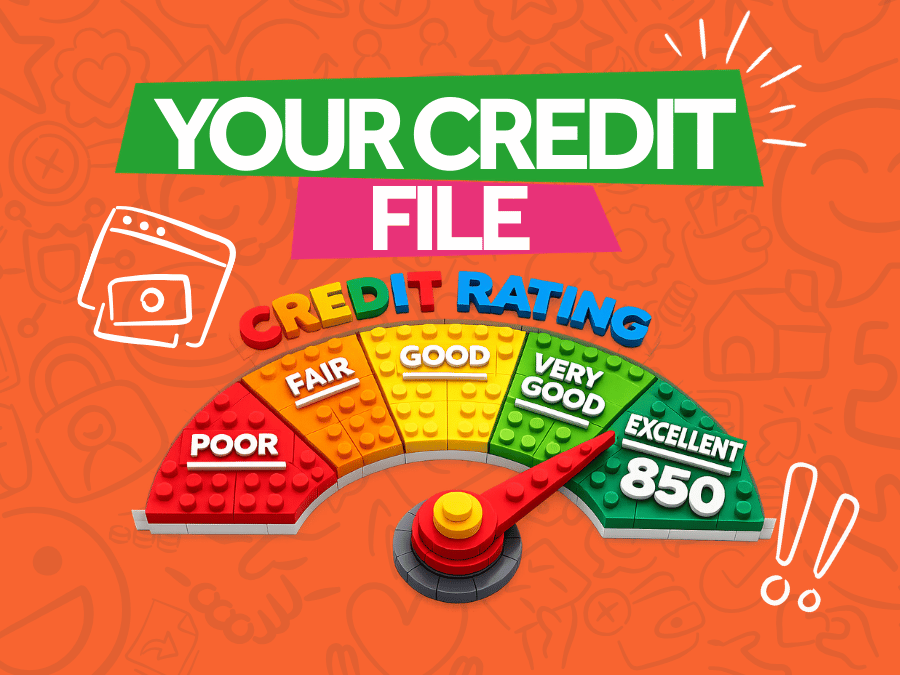

Managing debt well means staying on top of payments, not borrowing more than you can afford to repay, and understanding the terms of any loans or credit cards you have.

This helps build a good credit score, which is crucial for getting better interest rates on future loans or mortgages.

If You Don’t Understand, That’s Okay

Many people struggle with financial terms and concepts, like interest rates or APRs (annual percentage rates).

In the UK, a significant number of adults - 39%, or 20.3 million people—express a lack of confidence in managing their finances.

Shockingly, 11.5 million people have savings of less than £100 and nearly nine million people are struggling with serious debt, yet only about a third of them reach out for help.

These statistics show the challenges many face in understanding financial matters.

If you find yourself in a similar situation, it’s important to know that you’re not alone, and getting help can help you regain control and build a more secure financial future.

It’s okay not to know everything - what’s important is learning the basics that affect your everyday finances.

Managing Debt Responsibly

- Budgeting: Start by making a budget—a plan for how much money you have coming in and how much you need to spend. This helps you see where your money goes and avoid overspending.

- Credit Cards: Use them wisely by paying off the full balance each month if possible. This avoids interest charges and builds a positive credit history.

- Loans and Mortgages: Understand the terms before signing. Know how much you’ll pay each month, for how long, and what happens if you miss a payment.

There Is Help Out There…

Apps and websites can make managing money easier. They help with budgeting, tracking spending, and even managing debt.

IE Hub is completely free of charge, designed to simplify tracking your income and expenses, and debt management!

Once logged in, you’ll see your income, essential expenses, and what’s left for paying off any debts you may have.

If you want to share this with any company in hopes of reducing your payments, you can do so through your IE Hub portal. This removes any fears or anxieties that you may have around calling a lender yourself.

IE Hub can also help you discover any extra income opportunities and check if you qualify for special service provider tariffs.

Five key takeaways:

- The Basics: Debt involves borrowing money with an agreement to repay it later, often with interest. It includes various forms like credit cards, loans, and mortgages, used for big purchases or managing expenses.

- Perceptions: People perceive debt differently; some view any outstanding balance as a financial liability, while others see it as manageable credit when payments are consistent and planned.

- Problem Debt Indicators: Problem debt happens when people struggle with repayments, leading to arrears (missed payments) and potential default. It often results from financial challenges such as unexpected expenses or overspending.

- Managing Debt: Effective debt management involves budgeting to track income and expenses, using credit cards responsibly by paying off balances monthly, and understanding loan terms to avoid penalties and maintain good credit scores.

- Getting Help: Many people face financial uncertainty and lack confidence in managing money. Getting help through financial advice services or negotiating with creditors can prevent your debt from getting worse and provide pathways to financial stability.